March 09, 2026

Navigating Currency Trends and Capital Flows: Reflections on 2025

A year ago, when writing this piece, we made mention of the “sheer speed of change in a Maga-Part-Two world”. It feels fair to say that 2025 never slowed down and, given the start to this year, it seems as though 2026 has no intention of doing so either. Greenland, AI, Minnesota, Iran, Davos, tariffs on, tariffs off, Gold, de-dollarisation… all of these have hogged the headlines, been resolved or unresolved, reached record highs or dropped to multi-year lows, all in the space of a single month. The sheer amount of market-moving news, information dumping, and noise mischief-making is truly mind-boggling and, without getting too far into the existential realm, one can surely wonder just how long stable societies can continue to sustain this, let alone deal with even more.

Despite all the activity and uncertainty that last year brought, it was quite a stellar year for the Rand, starting 2025 at 18.88 and closing off at 16.55, a gain of 14%. For those wondering if this can, and will, continue, the following chart brings some good news: since the turn of the century, every year of significant Rand gains, as shown by the long red bars (the top of the bar shows where the Rand started the relevant year and the bottom where it ended the year), has been followed by another strong performance in the subsequent year. Of course, the drivers behind these moves have differed over the years (global vs domestic, economic/financial vs geopolitical, USD-driven vs ZAR-specific) and this chart does not act as a forecast; however, the pattern is worth noting. Put differently, ZAR bull rallies can typically run for 24+ months at a time – should this repeat, we may yet look forward to a year of 15.00 – 16.00 for ZAR/USD.

Investment Outflows

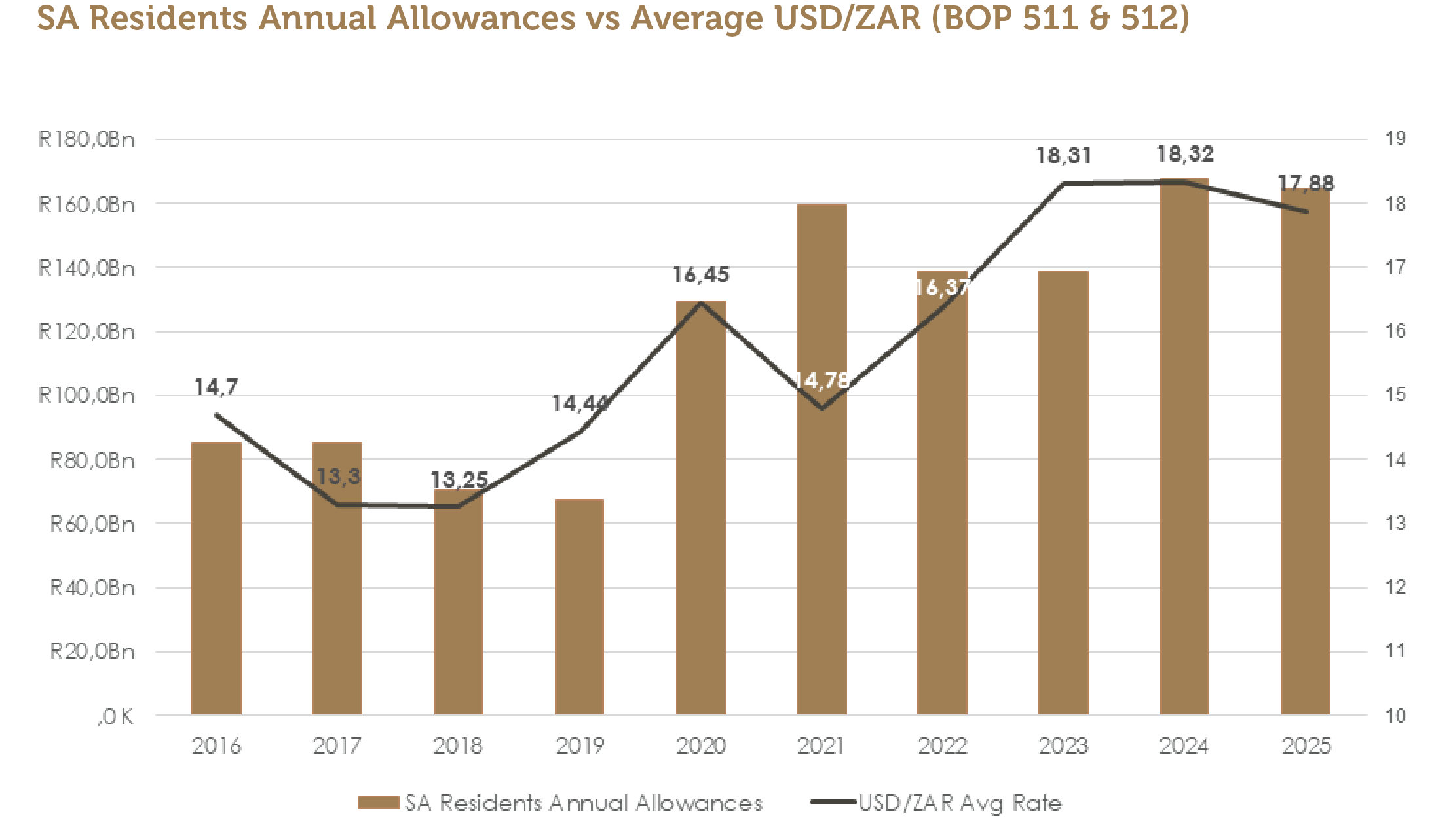

We typically view this category as discretionary offshore transactions, frequently intended for investment purposes. As such, these flows are often driven by local sentiment, the attractiveness of offshore investment opportunities and ZAR movements. In the face of a strengthening ZAR, one could therefore have expected such flows to increase, particularly during the second half of last year, during which most of the gains were made. The chart below, however, shows that this was not the case.

Part of the reason may be that the large 20% increase in such flows in 2024 compared to 2023 meant that a levelling-off was inevitable. We do get the sense, though, that the general improvement in sentiment towards South Africa, combined with global economic and political uncertainty and elevated equity market valuations, has perhaps reduced the sense of urgency and speed of decision-making when it comes to allocating capital offshore.

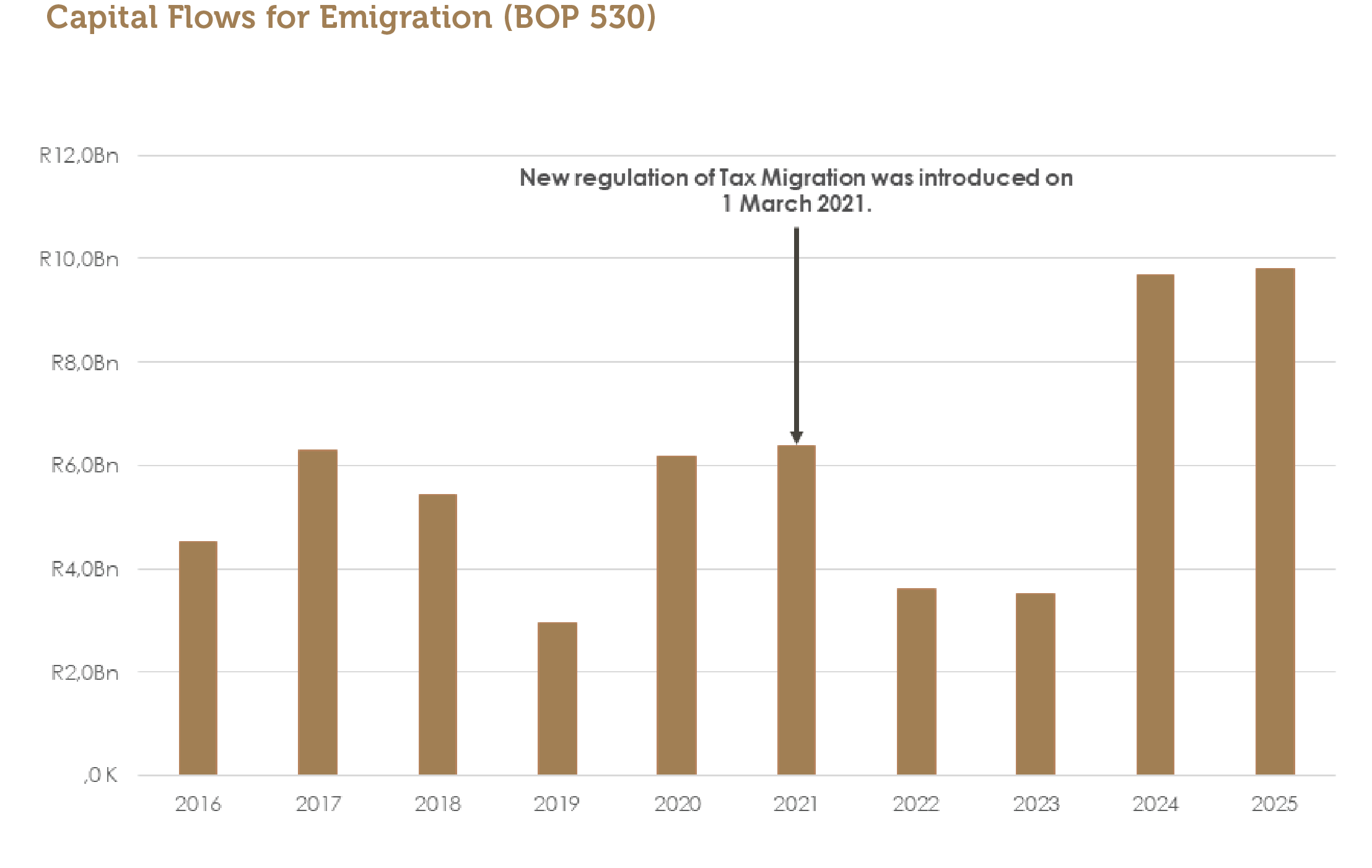

Tax Migration

Last year we mentioned that the increase in this category was likely due to the change in regulations regarding Tax Migration, introduced in March 2021. We said that “the ability of individuals who have ceased to be resident for an uninterrupted period of 3 years or longer, to access the full benefits of their non-voluntary investments, would have suddenly made a large of amount of such capital available for externalisation during the course of 2024.” Should this be the case, we may see these flows taper off somewhat, if not this year, then next.

Last year we mentioned that the increase in this category was likely due to the change in regulations regarding tax migration, introduced in March 2021. We said that “the ability of individuals who have ceased to be resident for an uninterrupted period of three years or longer to access the full benefits of their non-voluntary investments would have suddenly made a large amount of such capital available for externalisation during the course of 2024.” Should this be the case, we may see these flows taper off somewhat, if not this year, then next.

Inheritance Flows

Currency Partners frequently assists beneficiaries of inheritances to remit their funds abroad, be it via their resident allowances or in their capacities as non-residents or emigrants. While the nominal quantum of these flows will always remain small within the context of cross-border flows out of or into South Africa, this category has doubled since a few years ago and should continue steadily in the coming years. Beneficiaries of all ages have remitted inheritances through us over the past few years and, given the ongoing migration of younger generations, will likely continue doing so.

As one would expect, we find that the longer an individual has been out of South Africa, the less rate sensitive they become. Those who left more recently and still have a link to the country – be it family and friends still living here, a sense of familiarity with the situation in SA or a general affiinity towards their previous home – are more likely to be patient in waiting for an “attractive rate”.

This year, we include a chart showing inheritance capital flows into South Africa as well, which continue to demonstrate steady year-on-year growth.

Property Flows

Over the past five years, inward flows in this category have more than doubled, and there is little indication that this trend is going to slow down. Currency Partners facilitates large volumes of inward currency transactions for our wide international client base across the world. We are approached daily, either directly by the purchaser or via their Estate Agent or Conveyancer, to assist in securely and efficiently introducing their capital into the country.

It should not be surprising that the bulk of the deals we facilitate are for purchases in the Western Cape, which is often pointed to as a major contributor to ever-increasing property prices in Cape Town, Stellenbosch, Franschhoek and the surrounding areas, as well as further down the coast to George, Knysna and Plettenberg Bay. At some point, increased prices and a strengthening Rand may make property opportunities less attractive to foreigners… but it seems we are not there yet.

Tuition Flows

A relatively small category, this section serves as a reminder to clients that offshore tuition fees can be funded via this allowance, rather than one’s R1 million Single Discretionary Allowance. Provided the payer can supply an invoice made out to them from the relevant institution, together with the acceptance letter for the student named on the invoice, they need not use up their individual allowance on such payments.

Looking Ahead

There is little doubt that 2026 will continue to produce news and noise at the same pace and volume, if not greater, as what we have experienced over the past couple of years. There are simply too many large-scale political, economic, technological and societal disruptions currently underway for it to be otherwise. It remains to be seen – perhaps only decades from now as a study of the past – how a globalised, yet ununified World, reacts and adapts.

Still, within this context, cross-border transactions will continue to reflect the real-world requirements of individuals and corporates and we would therefore not expect any significant deviations or slow-down in the flows experienced last year.

To speak to an expert, please contact us at enquiries@currencypartners.co.za or +27 21 203 0081. We look forward to hearing from you and saving you money on the exchange rates.

SPEAK TO AN EXPERT